Every piece of equipment, vehicle, and machine your business owns was worth more the day you bought it than it is today. This steady loss of value is not a flaw in your accounting — it is a fundamental principle called depreciation, and how you account for it directly affects your profit figure, your tax position, and the accuracy of your balance sheet. For SME owners and accountants alike, understanding the main depreciation methods — and knowing which one to apply — is one of the most practically useful skills in the accounting toolkit.

What Is Depreciation and Why Does It Matter?

When a business buys a long-term asset — a delivery van, a piece of machinery, a computer server — it does not expense the full cost in the year of purchase. Instead, it spreads that cost over the asset’s useful working life. This spreading of cost is depreciation.

There are two core reasons this matters. First, it gives a truer picture of profitability. If you expensed a £40,000 van in full the year you bought it, your profit that year would appear artificially low. By depreciating it over five years at £8,000 per year, each year’s accounts reflect the actual consumption of that asset’s value. Second, the accumulated depreciation reduces the carrying value of the asset on your balance sheet — keeping it aligned with economic reality rather than overstating what the business actually owns.

Depreciation is a non-cash expense. It reduces profit and therefore reduces the tax liability, but no cash leaves the business at the point the depreciation charge is recorded. Cash only left when the asset was originally purchased.

The Main Methods of Depreciation

There are three methods you will encounter most frequently in practice. Each produces a different pattern of annual charges, and each suits different types of asset.

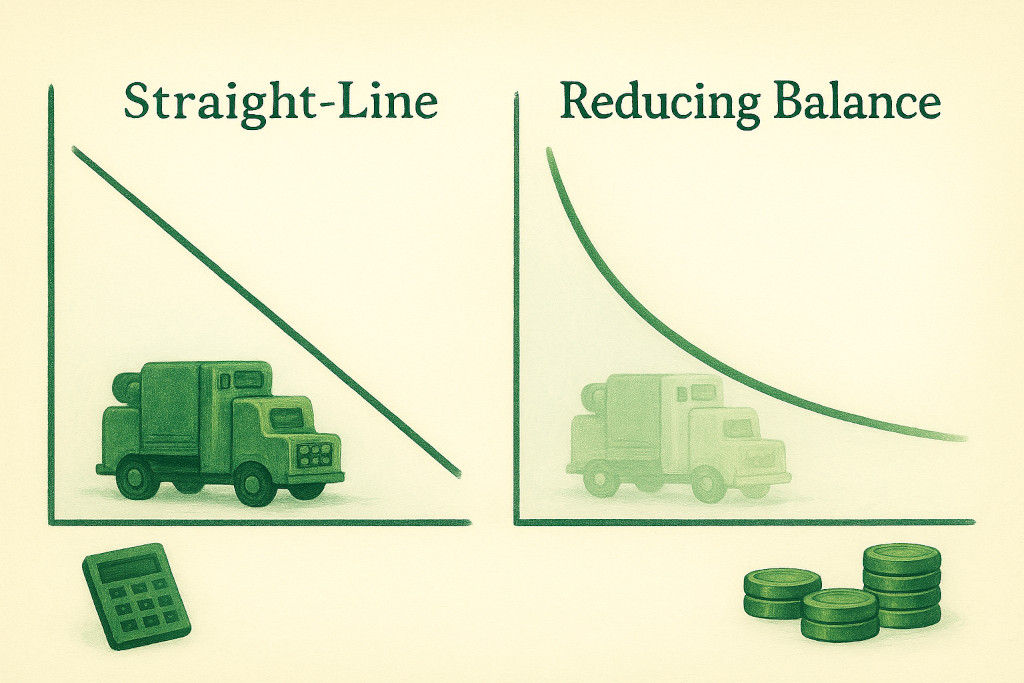

1. Straight-Line Depreciation

The simplest and most widely used method. The asset loses the same fixed amount of value each year over its useful life.

Formula: Annual Depreciation = (Cost − Residual Value) ÷ Useful Life (years)

The residual value (sometimes called scrap value) is the estimated amount the asset will be worth at the end of its useful life. If an asset will be worthless at disposal, residual value is zero.

2. Reducing Balance Depreciation

Also called the declining balance method. The depreciation charge is calculated as a fixed percentage of the asset’s remaining book value each year — not its original cost. This means the charge is higher in early years and tapers off over time, which better reflects how many assets (especially technology and vehicles) lose value more quickly when new.

Formula: Annual Depreciation = Net Book Value at Start of Year × Depreciation Rate %

3. Units of Production (Activity-Based) Depreciation

Rather than spreading cost over time, this method ties depreciation to actual usage. It is best suited to assets whose wear is genuinely driven by how much they are used — a printing press, a quarry vehicle, or specialised manufacturing equipment.

Formula: Depreciation per Unit = (Cost − Residual Value) ÷ Estimated Total Units of Production

Annual Charge = Depreciation per Unit × Units Produced in the Year

Worked Example: Comparing the Three Methods

Ashford Printing Ltd purchases a digital press for £50,000. It has an estimated useful life of five years and a residual value of £5,000. In a typical year the press handles approximately 200,000 print runs; total estimated lifetime output is 1,000,000 print runs. The table below shows Year 1 and Year 3 charges under each method.

| Method | Year 1 Charge (£) | Year 2 Charge (£) | Year 3 Charge (£) | Year 4 Charge (£) | Year 5 Charge (£) | Total (£) |

|---|---|---|---|---|---|---|

| Straight-Line (20%) | 9,000 | 9,000 | 9,000 | 9,000 | 9,000 | 45,000 |

| Reducing Balance (30%) | 15,000 | 10,500 | 7,350 | 5,145 | 3,602 | 41,597* |

| Units of Production (200k/yr) | 9,000 | 9,000 | 9,000 | 9,000 | 9,000 | 45,000 |

*Reducing balance at 30% leaves a residual book value of approximately £8,403 after five years. The rate would typically be set to bring the asset to its expected residual value — the figures above illustrate the pattern rather than an exact match.

Notice how the reducing balance method front-loads the expense: Ashford records a £15,000 charge in Year 1 versus £9,000 under straight-line. By Year 3, the reducing balance charge (£7,350) has dropped below the straight-line equivalent. This can have meaningful effects on reported profit — and therefore tax — in the early years of an asset’s life.

The depreciation method you choose does not change the total cost of the asset over its life — only the timing of when that cost hits your profit and loss account. Consistency and transparency in your chosen approach matter more than which method you pick.

Choosing the Right Method for Your Asset

No single method suits every asset. The key question is: how does this asset actually lose its value?

Use straight-line when the asset provides roughly equal benefit each year — office furniture, leasehold improvements, most computer equipment, and commercial property fixtures are good candidates. It is predictable, easy to explain to stakeholders, and administratively simple.

Use reducing balance for assets that decline in value rapidly when new — vehicles are the classic example. A van bought for £25,000 might lose £8,000 of market value in its first year, but only £3,000 in its fourth year. The reducing balance method aligns the accounting charge with this economic reality, producing a smoother match between the asset’s book value and its market value.

Use units of production for assets where utilisation, not time, is the primary driver of wear — heavy plant, specialist manufacturing tools, or mining equipment. If the machine sits idle for six months, no depreciation charge is recorded, which is a more accurate reflection of what happened economically.

Once chosen, the method should be applied consistently across similar asset classes and disclosed in the accounting policies note of your financial statements. Changing method without good reason raises questions with auditors and HMRC alike.

Depreciation, Residual Value, and Useful Life: The Key Estimates

Depreciation calculations rest on two estimates that require professional judgement: useful life and residual value. Both should reflect the business’s genuine expectations, not a default figure.

Useful life varies significantly by asset type. HMRC’s capital allowance rules provide a tax-focused view, but accounting depreciation and tax depreciation are separate concepts — a business may depreciate an asset over seven years for accounting purposes while claiming capital allowances under a different rate for tax. The difference creates timing differences that, in some cases, give rise to a deferred tax liability. (Our post on deferred tax covers this in detail.)

Residual value should be reviewed periodically. If market conditions change — for example, a particular model of vehicle loses value more rapidly than expected due to changing emissions regulations — the residual value estimate should be revised, and the remaining depreciation recalculated over the remaining useful life.

Depreciation treatment also varies depending on which accounting standards a business follows. Under IFRS (IAS 16), businesses have the option to revalue certain fixed assets to fair value and then depreciate from the revalued amount — a treatment not available under UK GAAP’s FRS 102. BrizoConsol’s comparison of IFRS vs UK GAAP key differences in financial reporting is a useful reference if your business is considering which framework applies, particularly for groups with international subsidiaries.

Common Depreciation Mistakes to Avoid

- Applying a single method to all assets indiscriminately. A laptop and a quarrying truck have very different usage profiles. Using straight-line for everything is administratively convenient but may misrepresent the economics.

- Setting residual value to zero by default. Many assets retain meaningful value at end of use — vehicles, specialist tools, and plant equipment are often sold secondhand. Ignoring residual value overstates the annual depreciation charge.

- Forgetting to start depreciation in the month of acquisition. Some businesses depreciate a full year’s charge regardless of when an asset was bought. A pro-rata charge from the acquisition date is more accurate (and required under some standards).

- Continuing to depreciate fully depreciated assets. Once an asset reaches its residual value, depreciation stops. A nil net book value asset that is still in use should be disclosed as such — not written down further.

- Confusing accounting depreciation with tax depreciation (capital allowances). These are separate calculations. The accounting charge goes through your P&L; the capital allowance claim goes on your tax return. They rarely match in any given year.

Key Takeaways

- Depreciation spreads the cost of a long-term asset over its useful life, matching the expense to the periods that benefit from the asset’s use.

- The three main methods are straight-line (equal annual charge), reducing balance (front-loaded charge), and units of production (usage-based charge).

- Method choice should reflect how the asset actually loses value — not simply default to the simplest option.

- Two key estimates drive depreciation: useful life and residual value. Both require regular review.

- Accounting depreciation and tax capital allowances are separate calculations — differences between them can create deferred tax positions.

- Once chosen, apply your depreciation policies consistently and disclose them clearly in your financial statements.

Related reading: Depreciation appears as a line on your Income Statement and reduces the carrying value of assets on your Balance Sheet. When the timing difference between accounting depreciation and tax allowances creates a deferred tax balance, our guide to Deferred Tax Liability explains what that means and how it is recorded. For a broader overview of the financial frameworks your business may operate under, see our guide to IFRS.