Every number in every set of accounts — whether for a sole trader, a growing SME, or a listed corporation — was put there by a journal entry. Double-entry bookkeeping is the language accountants use to record financial events, and it has been in continuous use since the Italian merchants of the fifteenth century first formalised it. Understanding how it works does not require a degree in accounting. What it requires is grasping one simple idea: every transaction affects two accounts, always, and the two effects must balance. Get comfortable with that principle, and the entire structure of accounting becomes logical rather than mysterious.

What Is Double-Entry Bookkeeping?

Double-entry bookkeeping is a system in which every financial transaction is recorded as two equal and opposite entries — one debit and one credit — in different ledger accounts. The name comes from the fact that each transaction is entered twice: once on the debit side of one account, and once on the credit side of another.

This is not an arbitrary accounting convention. It reflects economic reality. When a business buys a van for cash, two things happen simultaneously: the business gains an asset (the van) and loses an asset (the cash). Recording both sides of this exchange is what makes the books balance. If you only recorded the van arriving but not the cash leaving, your accounts would be out of balance — and the discrepancy would be the first sign something was wrong.

The result of this system is that the total of all debits always equals the total of all credits. This self-balancing property is one of accounting’s most powerful error-detection mechanisms. When a trial balance — the summary of all account balances — does not balance, it signals immediately that an error has been made somewhere in the entries.

Debits and Credits: The Golden Rules

The single most common source of confusion in bookkeeping is the meaning of “debit” and “credit”. In everyday language, a debit means money going out of your bank account; a credit means money coming in. In double-entry bookkeeping, the words mean something more specific and often counterintuitive to beginners.

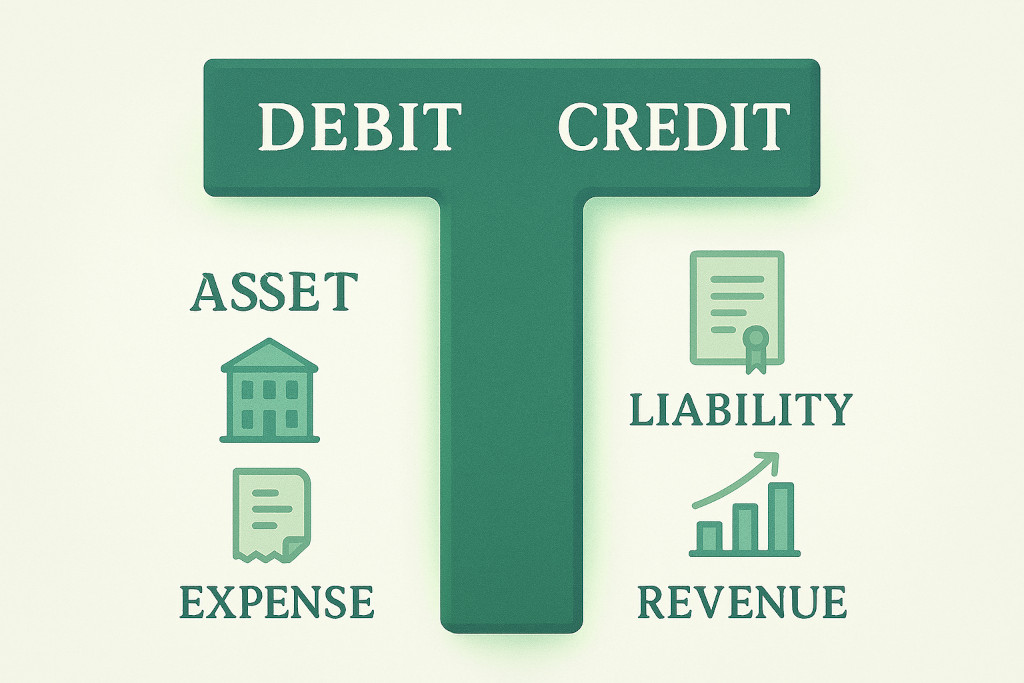

In accounting, every ledger account belongs to one of five categories: assets, liabilities, equity, income, or expenses. The rule for debits and credits is different depending on the category:

| Account Type | A Debit… | A Credit… | Example Account |

|---|---|---|---|

| Asset | Increases the balance | Decreases the balance | Cash, Trade Debtors, Vehicles |

| Liability | Decreases the balance | Increases the balance | Bank Loan, Trade Creditors, VAT Payable |

| Equity | Decreases the balance | Increases the balance | Share Capital, Retained Earnings |

| Income / Revenue | Decreases the balance | Increases the balance | Sales Revenue, Interest Received |

| Expense | Increases the balance | Decreases the balance | Wages, Rent, Depreciation |

A useful memory aid is DEAD CLIC: Debits increase Expenses, Assets, and Drawings; Credits increase Liabilities, Income, and Capital. Once this table is memorised, any transaction can be broken down logically into its two sides without guesswork.

Debits and credits are not value judgements — “debit” does not mean “bad” and “credit” does not mean “good”. They are simply the left and right sides of every ledger account. Their effect — whether they increase or decrease a balance — depends entirely on the type of account they are applied to.

Journal Entries in Practice: A Worked Example

Birchwood Consultants Ltd is a small consultancy. In October, the following transactions occur. Let us record each as a double-entry journal entry.

Transaction 1: Owner invests £20,000 into the business

| Account | Debit (£) | Credit (£) | Reason |

|---|---|---|---|

| Bank (Asset) | 20,000 | Cash received — asset increases | |

| Share Capital (Equity) | 20,000 | Owner’s investment — equity increases |

Transaction 2: Business pays £1,200 for office rent

| Account | Debit (£) | Credit (£) | Reason |

|---|---|---|---|

| Rent Expense (Expense) | 1,200 | Cost incurred — expense increases | |

| Bank (Asset) | 1,200 | Cash paid out — asset decreases |

Transaction 3: Business invoices a client £5,000 for consulting work

| Account | Debit (£) | Credit (£) | Reason |

|---|---|---|---|

| Trade Debtors (Asset) | 5,000 | Amount owed to us — asset increases | |

| Consulting Revenue (Income) | 5,000 | Revenue earned — income increases |

Transaction 4: Client pays the £5,000 invoice

| Account | Debit (£) | Credit (£) | Reason |

|---|---|---|---|

| Bank (Asset) | 5,000 | Cash received — asset increases | |

| Trade Debtors (Asset) | 5,000 | Debt cleared — asset decreases |

After all four transactions, the total of all debit entries (£31,200) equals the total of all credit entries (£31,200). The books balance. This is double-entry working as intended.

From Journal Entries to Financial Statements

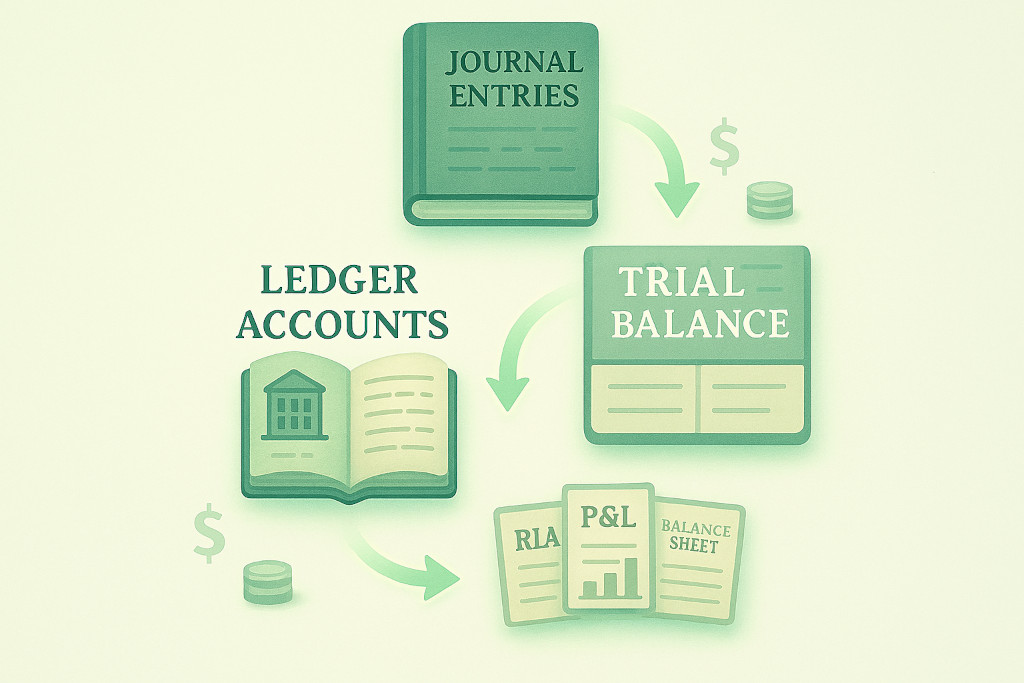

Journal entries do not live in isolation. They flow through a structured sequence that ultimately produces the financial statements every business relies on.

Each journal entry is first recorded in a journal (the book of original entry) in chronological order. The entries are then posted to individual ledger accounts — one account per category, such as “Bank”, “Rent Expense”, or “Trade Debtors”. Each ledger account is typically visualised as a T-account, with debits on the left and credits on the right, allowing the running balance to be tracked at a glance.

Periodically — usually at month-end — all ledger account balances are extracted into a trial balance. If the total of all debit balances equals the total of all credit balances, the bookkeeping is arithmetically correct. The trial balance then feeds directly into the preparation of the three core financial statements: the income statement (profit and loss), the balance sheet, and the cash flow statement.

This chain — from individual transaction to financial statement — is the same whether you are using a paper ledger, a spreadsheet, or modern accounting software like Xero or QuickBooks. The software automates the posting and trial balance, but every entry it makes follows the same double-entry logic. For businesses that operate across multiple entities, the same principle applies at the consolidation stage: group accountants must understand the underlying journal entries in each subsidiary in order to correctly eliminate intercompany transactions and produce accurate group accounts. BrizoConsol’s guide on delivering consolidated financials without the manual work explains how this aggregation process works in practice for multi-entity groups.

Common Journal Entry Types for SMEs

While every transaction is unique, most SME bookkeeping involves a relatively small set of recurring entry types. Becoming fluent with these covers the vast majority of day-to-day accounting:

- Sales invoice raised: Debit Trade Debtors / Credit Sales Revenue

- Customer payment received: Debit Bank / Credit Trade Debtors

- Purchase invoice received: Debit Expense or Asset / Credit Trade Creditors

- Supplier payment made: Debit Trade Creditors / Credit Bank

- Wages paid: Debit Wages Expense / Credit Bank

- Depreciation charged: Debit Depreciation Expense / Credit Accumulated Depreciation

- Prepayment (e.g. insurance paid in advance): Debit Prepayment Asset / Credit Bank; then reverse monthly as expense accrues

- Accrual (e.g. electricity bill not yet received): Debit Electricity Expense / Credit Accruals (Liability)

- Loan received: Debit Bank / Credit Loan Liability

- Dividend paid: Debit Retained Earnings / Credit Bank

The accruals and prepayments entries in particular are central to the accruals basis of accounting — the principle that income and expenses are recognised when they are earned or incurred, not simply when cash changes hands. This is what separates proper financial accounting from simple cashbook recording, and it is what makes financial statements meaningful for decision-making rather than merely a record of bank movements.

Key Takeaways

- Double-entry bookkeeping records every transaction as two equal and opposite entries — a debit in one account and a credit in another.

- Debits increase assets and expenses; credits increase liabilities, equity, and income. The mnemonic DEAD CLIC helps: Debits increase Expenses, Assets, Drawings; Credits increase Liabilities, Income, Capital.

- The system is self-balancing: total debits always equal total credits. A trial balance that does not balance signals a bookkeeping error.

- Journal entries flow through ledger accounts and a trial balance before becoming the income statement, balance sheet, and cash flow statement.

- Most day-to-day SME bookkeeping involves ten or so recurring entry types. Mastering these covers the overwhelming majority of transactions a business will encounter.

- Accounting software automates the posting and trial balance, but the underlying double-entry logic is identical — understanding it makes you a more confident and critical user of any accounting system.

Related reading: Double-entry bookkeeping is the mechanism that keeps the Accounting Equation (Assets = Liabilities + Equity) permanently in balance. The ledger accounts for assets and liabilities flow directly into the Balance Sheet, while income and expense accounts form the Income Statement. For a broader introduction to the discipline that connects all of these concepts, see our post on Accounting Made Simple.