A profitable business can still run out of cash — and that is one of the most common reasons small businesses fail. The cash flow statement is the financial report that cuts through the noise and shows whether money is actually moving in and out of your business, separate from accounting profit. If you can read it confidently, you hold one of the most powerful diagnostic tools in finance.

This guide walks you through each section of the cash flow statement, how to read it, and what warning signs to watch for.

What Is a Cash Flow Statement?

The cash flow statement — formally called the Statement of Cash Flows — is one of the three core financial statements, alongside the income statement and the balance sheet. Where the income statement tells you whether the business is profitable, and the balance sheet shows what it owns and owes at a point in time, the cash flow statement answers a simpler question: where did the cash come from, and where did it go?

Under both IFRS (IAS 7) and US GAAP (ASC 230), companies are required to include a statement of cash flows in their financial reporting. It covers a defined reporting period — typically a quarter or a full financial year.

Why this mattersA company can report healthy net profit on its income statement while simultaneously draining cash. This happens when revenue is recognised before cash is received — a feature of accrual accounting. The cash flow statement reveals this gap, showing the real liquidity position behind the reported numbers.

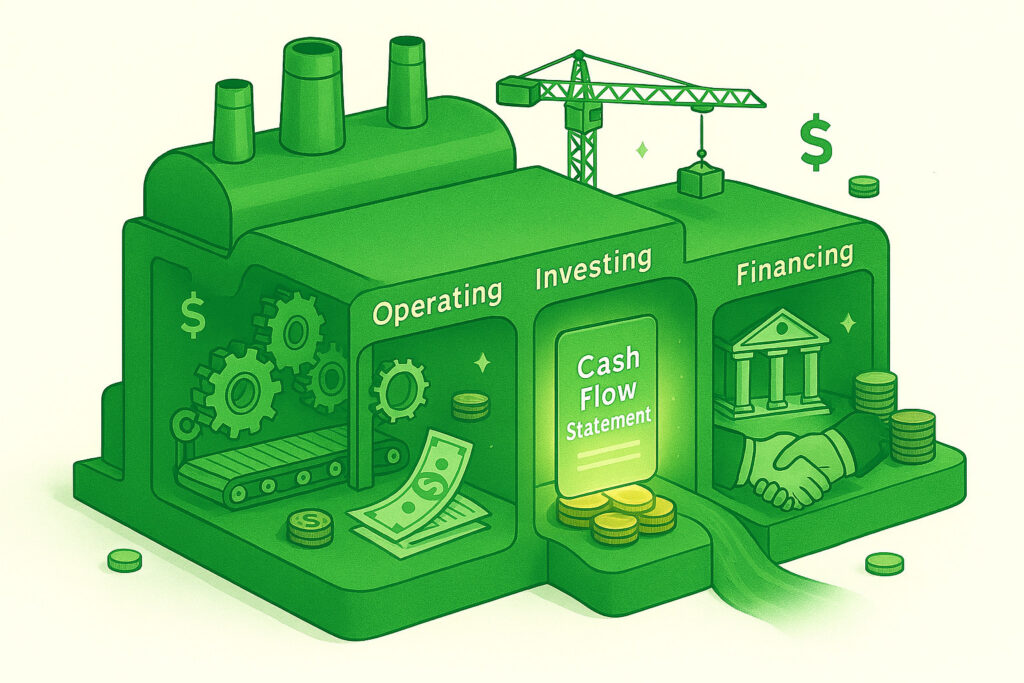

The Three Sections of a Cash Flow Statement

Every cash flow statement is divided into three sections. Each one tells a different part of the story.

Operating Activities

This section covers cash generated or consumed by the core business — selling goods or services, paying suppliers, covering wages, and settling taxes. It is the most telling section, because it shows whether the business model is self-sustaining without relying on external funding or asset sales.

Typical items include cash received from customers, cash paid to suppliers and employees, interest paid, and income tax paid.

Investing Activities

Investing cash flows show how the business deploys capital for long-term growth — buying or selling property, equipment, or other businesses. A negative figure here is not automatically bad; it often means the company is actively investing in its future capacity.

Common items include purchase of property and equipment (capital expenditure), proceeds from asset sales, and acquisitions.

Financing Activities

This section tracks how the business raises and repays capital. It covers borrowing, loan repayments, share issuances, and dividends paid to shareholders. For groups with multiple entities, the financing section can become more complex — intercompany loans, for example, need to be eliminated when preparing consolidated statements. BrizoConsol has a useful explainer on why intercompany transactions are eliminated in consolidation if that applies to your situation.

A Worked Example: Maple Goods Ltd

Below is a simplified cash flow statement for a fictional SME, Maple Goods Ltd, for the year ended 31 December 2025.

| Line Item | £000 |

|---|---|

| Operating Activities | |

| Cash received from customers | 1,840 |

| Cash paid to suppliers | (960) |

| Cash paid to employees | (420) |

| Income tax paid | (55) |

| Net cash from operating activities | 405 |

| Investing Activities | |

| Purchase of equipment | (250) |

| Proceeds from sale of old vehicle | 18 |

| Net cash used in investing activities | (232) |

| Financing Activities | |

| Loan repayment | (80) |

| Dividends paid | (30) |

| Net cash used in financing activities | (110) |

| Net increase in cash and equivalents | 63 |

| Opening cash balance | 142 |

| Closing cash balance | 205 |

Maple Goods Ltd generated a solid £405k from its core operations, invested £232k back into the business, and met all its financing obligations — ending the year £63k richer in cash. This is a healthy, sustainable pattern: operations fund everything else.

Direct vs Indirect Method: What Is the Difference?

There are two ways to present the operating activities section. The investing and financing sections are always presented the same way — only operating activities differ between methods.

The direct method lists actual cash receipts and payments — cash in from customers, cash out to suppliers, and so on. It is more transparent and easier to understand at a glance. IFRS encourages this approach but permits either.

The indirect method starts with net profit and adjusts for non-cash items (such as depreciation and amortisation) and changes in working capital (receivables, payables, inventory). This is the most commonly used method in practice because it ties directly back to the income statement and is faster to prepare from standard accounting records.

The example above uses the direct method. Most published company accounts use the indirect method — always check the notes to confirm which is applied when reading external financial statements.

How to Analyse a Cash Flow Statement

Once you can read the statement, the next step is knowing what to look for. Here are five key questions to ask.

- Is operating cash flow positive? A consistently negative operating cash flow is a warning sign — the business is burning cash on its core operations and relying on external funding or asset sales to survive.

- How does operating cash flow compare to net profit? If profit is high but operating cash flow is low, look for rising receivables or inventory — cash is being trapped in the working capital cycle rather than landing in the bank.

- Is investing activity appropriate for the stage of the business? Heavy capital expenditure in a growing company is expected. In a declining one, continued capex without matching revenue growth is a concern.

- Is financing sustainable? A business that constantly raises new debt or equity to fund day-to-day operations is not self-sufficient. Healthy businesses fund operations from operations.

- What is the free cash flow? Free Cash Flow = Operating Cash Flow minus Capital Expenditure. This is the cash left over after maintaining and growing the asset base — the truest measure of a business’s cash generation for investors and lenders.

For businesses operating across multiple entities or currencies, cash flow analysis gets more complex. Currency translation differences, for instance, can affect how cash balances are reported at group level. BrizoConsol’s guide on calculating the Cumulative Translation Adjustment in group consolidation covers this in detail.

Common Mistakes to Avoid

Even experienced managers misread cash flow statements. These are the most common pitfalls.

Confusing profit with cash. Accrual accounting means you can invoice a client today and wait 90 days for payment. Reported profit goes up the moment the invoice is raised; cash does not arrive until payment is received. Always track these separately.

Ignoring the timing of cash flows. A seasonal business may be highly profitable on an annual basis but dangerously cash-thin during off-peak months. Cash flow forecasting — looking forward — is just as important as reading historical statements.

Overlooking working capital signals. Growing receivables or inventory can silently drain cash even as profits rise. In the indirect method, these movements appear explicitly in the operating section. Pay close attention to them.

Treating all capex as straightforwardly positive. Capital expenditure consumes real cash today. A business that over-invests in assets without matching revenue growth can become cash-constrained despite healthy reported profits.

Key takeawayThe cash flow statement is not a standalone document — it works best read alongside the income statement and the balance sheet. The three together give you a complete picture of financial health: profitability, net worth, and liquidity.

Summary: Key Points to Remember

- The cash flow statement has three sections: operating, investing, and financing activities.

- A profitable business can still fail if it runs out of cash — this report reveals that risk.

- Strong, positive operating cash flow is the hallmark of a financially self-sustaining business.

- The indirect method (most common) starts with net profit and adjusts for non-cash items and working capital movements.

- Free Cash Flow = Operating Cash Flow − Capital Expenditure. It is the clearest measure of cash generation available to reinvest or return to shareholders.

- Always read all three financial statements together for a complete view.

Related reading on Accounting Reports Daily:

Accounting Basics: The Balance Sheet — Structure and Key Elements

International Financial Reporting Standards (IFRS): A Complete Guide

Understanding Funding in Accounting: Shares, Debts, and Financing Options

Comments

One response to “Understanding the Cash Flow Statement: Your Business’s Financial Pulse”

[…] reading: For a deeper look at how cash flows through your business, see our guide to Understanding the Cash Flow Statement. If you want to project your cash position forward, our Cash Flow Forecasting for […]