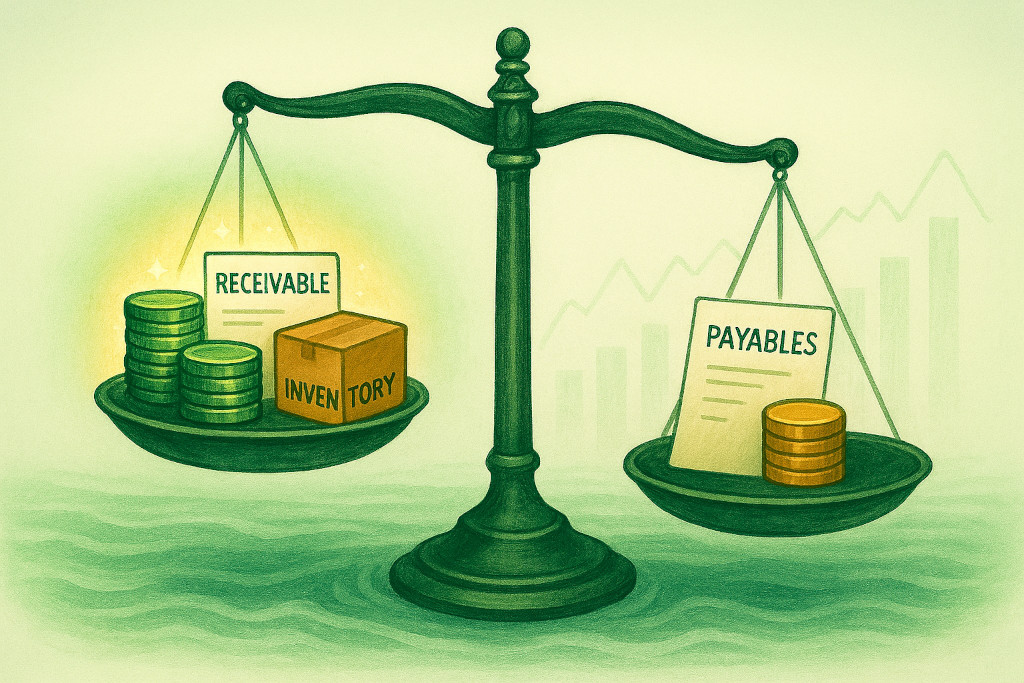

If your business has ever waited on a customer to pay an invoice — or had a supplier chasing you for settlement — you have already experienced accounts receivable and accounts payable in action. These two concepts sit at the heart of everyday business finance, yet many SME owners treat them as administrative details rather than the cash flow levers they actually are. Understanding both, and managing them actively, is one of the most direct ways to improve your business’s financial health without changing a single line of your P&L.

What Is Accounts Receivable?

Accounts receivable (AR) is the money your customers owe you for goods or services you have already delivered but not yet been paid for. When you issue an invoice to a customer on credit terms — say, 30 days to pay — that outstanding amount sits in your accounts receivable until settlement arrives.

On your balance sheet, accounts receivable appears as a current asset. It represents real value your business has earned but not yet collected. The distinction matters: revenue is recognised when the sale is made (or the service delivered), but cash only arrives when the customer actually pays. A business with strong sales but slow-paying customers can find itself in a cash squeeze even when its P&L looks healthy.

Common examples of accounts receivable include unpaid client invoices in a professional services firm, outstanding balances from wholesale customers in a product business, and accrued revenue for ongoing service contracts billed in arrears.

What Is Accounts Payable?

Accounts payable (AP) is the mirror image: the money your business owes to its own suppliers and vendors for goods or services you have received but not yet paid for. When a supplier delivers stock and gives you 45 days to settle the invoice, that liability sits in your accounts payable until you make the payment.

Accounts payable appears on the balance sheet as a current liability. Unlike accounts receivable — which you want to collect as quickly as possible — accounts payable can be managed strategically. Paying on the last day of your agreed credit terms, rather than immediately, preserves cash in your business for longer. That said, paying late risks supplier relationships and can result in penalties or lost credit terms.

Common examples include invoices from raw material suppliers, outstanding bills from service providers such as IT support or cleaning contractors, and utilities bills not yet settled.

AR vs AP at a Glance

| Feature | Accounts Receivable (AR) | Accounts Payable (AP) |

|---|---|---|

| Definition | Money customers owe your business | Money your business owes suppliers |

| Balance sheet position | Current asset | Current liability |

| Cash flow direction | Cash flowing in (when collected) | Cash flowing out (when paid) |

| Goal | Collect as quickly as possible | Pay on time — not early, not late |

| Risk if mismanaged | Cash shortfall; bad debts | Damaged supplier relationships; late fees |

| Key metric | Days Sales Outstanding (DSO) | Days Payable Outstanding (DPO) |

| Who manages it | Finance team; credit control | Finance team; procurement |

The Key Metrics: DSO and DPO

Two numbers tell you more about your AR and AP performance than anything else: Days Sales Outstanding (DSO) and Days Payable Outstanding (DPO).

Days Sales Outstanding (DSO) measures the average number of days it takes your customers to pay after an invoice is issued. The formula is:

DSO = (Accounts Receivable ÷ Total Credit Sales) × Number of Days

For example, if your accounts receivable balance is £120,000 and your total credit sales over the past 90 days were £360,000, your DSO is (120,000 ÷ 360,000) × 90 = 30 days. If your standard payment terms are 30 days, that is healthy. If your terms are 14 days, you have a problem.

Days Payable Outstanding (DPO) measures the average number of days your business takes to pay its own suppliers. The formula is:

DPO = (Accounts Payable ÷ Cost of Goods Sold) × Number of Days

A higher DPO means you are holding onto cash for longer before paying out — which is beneficial for liquidity, provided you are still settling within agreed terms. An unusually high DPO can signal cash flow strain or strained supplier relationships.

The gap between your DSO and DPO is one of the most revealing numbers in your business. If customers take 60 days to pay you but you must pay suppliers in 30, you are permanently funding a 30-day cash shortfall out of your own resources.

Best Practices for Managing Accounts Receivable

Active AR management is one of the highest-return activities in a small business. The following practices make a tangible difference:

- Invoice promptly. Every day between completing a job and raising the invoice is a day added to your DSO for free. Invoice on completion, or on a regular billing cycle, without delay.

- Set clear credit terms. State your payment terms explicitly on every invoice — “Payment due within 30 days of invoice date” — and include bank details. Ambiguity gives customers an excuse for delay.

- Send payment reminders proactively. A polite reminder three to five days before the due date, and another on the due date itself, catches inadvertent delays before they become disputes.

- Review your aged debtors list weekly. An aged debtors report shows outstanding invoices grouped by how long they have been open (0–30 days, 31–60 days, 61–90 days, 90+ days). Any balance in the 60+ column needs active attention.

- Assess creditworthiness before extending credit. For new customers placing large orders on credit terms, a basic credit check or trade reference request is worth the small effort.

- Consider early payment incentives. A 1–2% discount for payment within ten days can accelerate cash collection significantly where margins allow.

Best Practices for Managing Accounts Payable

AP management is less about speed and more about discipline and relationships:

- Pay on the last day of agreed terms — not before, not after. Early payment gifts your cash to suppliers unnecessarily. Late payment risks penalties and can damage the relationship or lose you preferential terms.

- Centralise invoice approval. A clear approval process — who can authorise which values, and within what timeframe — prevents invoices sitting unprocessed on people’s desks.

- Reconcile supplier statements monthly. Matching your accounts payable ledger against supplier statements catches duplicate invoices, missed credits, and disputed charges before they compound.

- Negotiate payment terms actively. Standard supplier terms are a starting point, not a fixed rule. As your relationship and order volume grows, 45- or 60-day terms are often available and worth asking for.

- Watch for duplicate payments. In businesses where invoices arrive through multiple channels, duplicate payments are a surprisingly common drain on cash. A simple purchase order matching process prevents most of them.

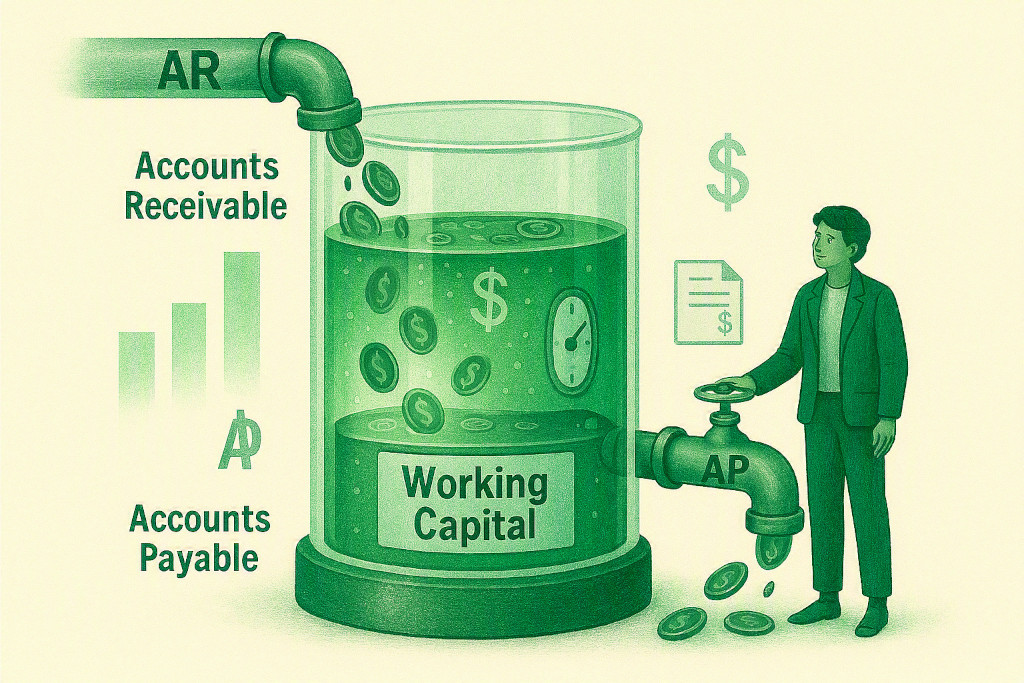

How AR and AP Affect Working Capital

Accounts receivable and accounts payable are the two most active drivers of working capital — the net current assets available to fund your day-to-day operations. Working capital is broadly calculated as current assets minus current liabilities, and AR and AP sit on either side of that equation.

Reducing DSO increases working capital: collecting cash faster means more is available. Increasing DPO (within agreed terms) also increases working capital: keeping cash in the business longer before paying it out provides a buffer. Our guide on working capital management for SMEs covers how these levers interact with inventory and the broader cash conversion cycle.

For businesses operating across multiple entities, intercompany AR and AP add another layer of complexity. When one group entity sells to another, an accounts receivable balance arises in the selling entity and a matching accounts payable balance arises in the buying entity. These must be eliminated in consolidated accounts to avoid overstating both assets and liabilities. BrizoConsol’s guide on automated intercompany journals explains how this elimination process works in practice and how to reduce the manual effort involved at month-end close.

A Worked Example: DSO in Action

To make DSO concrete, consider a marketing agency with the following figures:

| Item | Amount |

|---|---|

| Accounts receivable balance at month-end | £85,000 |

| Total credit revenue over the past 60 days | £200,000 |

| DSO calculation | (£85,000 ÷ £200,000) × 60 days = 25.5 days |

| Standard payment terms offered | 30 days |

| Assessment | DSO is within terms — AR management is healthy |

If the same agency found its DSO creeping to 48 days while its terms remained 30, that 18-day gap represents approximately £60,000 in cash that should have arrived but has not. At that point, reviewing the aged debtors list, identifying which clients are consistently late, and tightening credit control processes becomes urgent.

Key Takeaways

- Accounts receivable is money owed to your business (current asset); accounts payable is money owed by your business (current liability).

- DSO measures how quickly customers pay; DPO measures how long you take to pay suppliers. Both directly affect your cash position.

- The gap between DSO and DPO is a structural cash flow gap your business must fund — narrowing it improves liquidity without touching your P&L.

- Prompt invoicing, clear payment terms, aged debtor reviews, and proactive reminders are the core of good AR management.

- For AP, the goal is disciplined payment on agreed terms — not early, not late — and regular reconciliation of supplier accounts.

- In multi-entity businesses, intercompany AR and AP balances must be eliminated in consolidated accounts to present an accurate group picture.

For related reading, see our guides on working capital management, cash flow forecasting for SMEs, key financial ratios, and understanding the cash flow statement.